Should I Buy a House Now or Wait in Little Rock?

A straight answer for buyers in Little Rock, North Little Rock, Sherwood, and Maumelle trying to decide whether today’s prices, rates, inventory, and monthly payments actually make sense.

The honest answer is this: you should buy a house now if the payment works, your income is stable, you have enough cash reserves, and you plan to stay in the home long enough for ownership to make financial sense.

You should probably wait if you are stretching your budget, your job or income is uncertain, you do not have enough money left after closing, or you are hoping the market will fix an affordability problem that your numbers do not support.

That may not be the answer people want, but it is the answer people need.

In the Little Rock real estate market, the question is not just, “Are prices going up or down?” The better question is, “Does this specific house make sense for my life, my payment, my timeline, and my risk tolerance?”

That is where a lot of buyers get in trouble. They try to time the market instead of running the numbers.

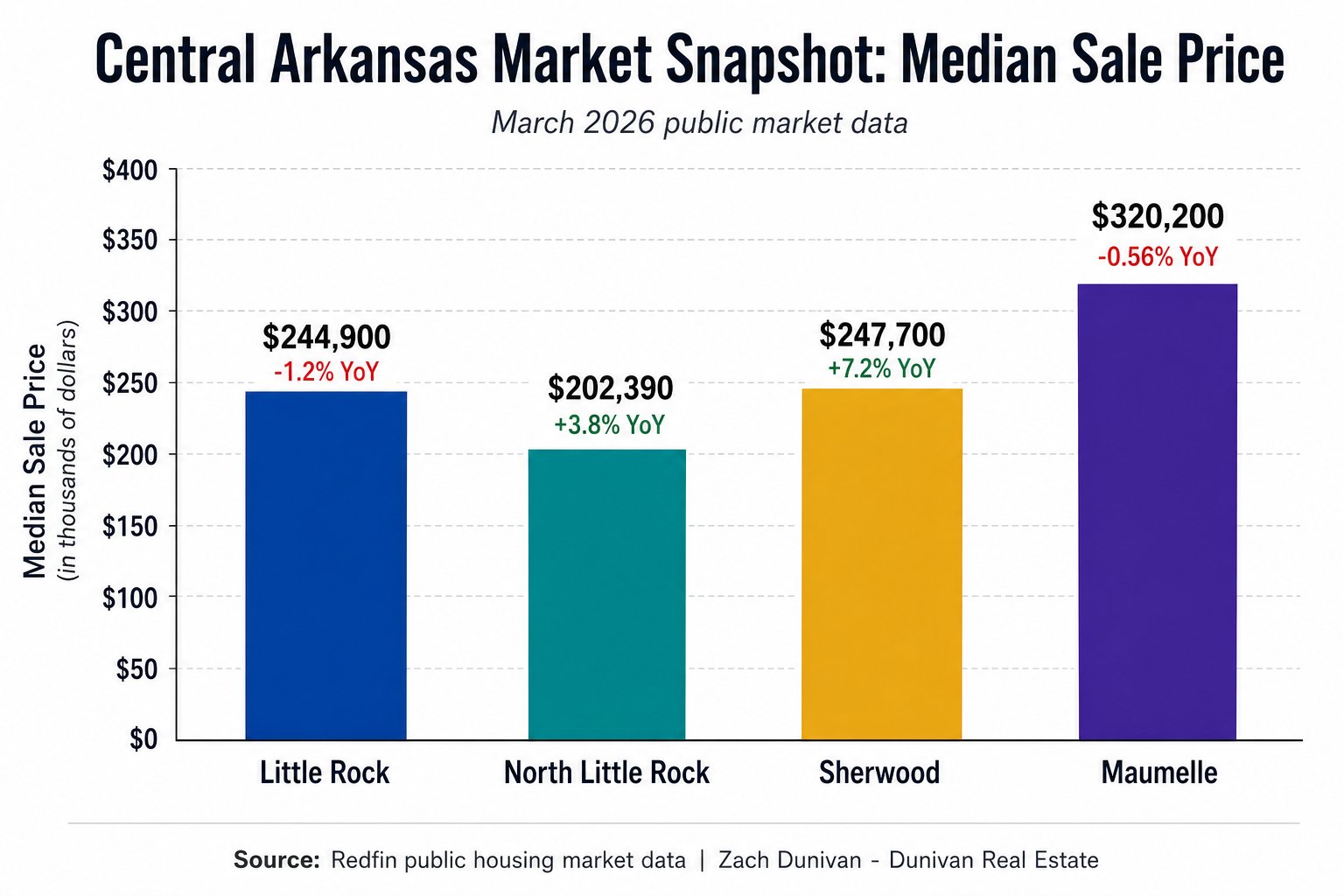

The public market data tells a pretty clear story. This is not a crash market. It is also not a market where buyers should blindly overpay. Little Rock, North Little Rock, Sherwood, and Maumelle are each moving differently, and that matters.

Little Rock’s median sale price was around $265,000 over the most recent three-month period, up 6.6% from the same time last year. North Little Rock’s March 2026 median sale price was around $202,390, up 3.8% year over year, but homes were averaging 101 days on market. Sherwood’s March 2026 median sale price was around $247,700, up 7.2% year over year, with homes averaging 59 days on market. Maumelle’s March 2026 median sale price was around $320,200, slightly down 0.56% year over year, with homes averaging 65 days on market.

That tells me this is a property-by-property market.

Some homes are still moving. Some are sitting. Some sellers have leverage. Some buyers have room to negotiate. It depends on the house, the price, the condition, the location, the financing, and how realistic both sides are.

That is why the decision to buy now or wait needs to be based on math, not headlines.

Should I buy a house now or wait in Little Rock?

You should buy now if the house fits your budget, you have stable income, you have enough money left after closing, and you plan to stay in the home long enough for ownership to make sense.

You should wait if the payment feels uncomfortable, you are depending on future rate drops to make the home affordable, you have no cash cushion, or you may need to move again quickly.

That is the real answer.

Buying a house is not just about qualifying for a loan. Qualifying means a lender says you can technically buy the home. It does not always mean the home is the smartest financial move for you.

Before buying, you need to know your full monthly payment, including principal, interest, taxes, insurance, mortgage insurance if applicable, HOA dues if there are any, utilities, maintenance, and the cost of actually living in the home.

A house can look affordable at the purchase price and still become stressful once the real monthly numbers are added up.

That is why I do not like giving generic advice like, “Now is always a good time to buy.” That is not true for everybody.

For the right buyer, now may be a great time. For the wrong buyer, now may be a mistake.

What does the current market data say?

The Central Arkansas market is not moving as one single market. Little Rock, North Little Rock, Sherwood, and Maumelle each tell a different story.

Little Rock is showing price growth, with the median sale price around $265,000 over the most recent three-month period, up 6.6% year over year. That does not mean every house in Little Rock is overpriced or underpriced. It means the overall market has continued to show value growth, but buyers still need to look closely at the specific neighborhood, condition, and competition.

North Little Rock is more affordable on paper, with a March 2026 median sale price around $202,390. Prices were up 3.8% year over year, but homes were averaging 101 days on market. That tells me buyers may have more room to negotiate on certain properties, especially homes that have been sitting, need work, or are priced too aggressively.

Sherwood is showing stronger movement, with a March 2026 median sale price around $247,700, up 7.2% year over year. Homes were averaging 59 days on market, which is much faster than North Little Rock. That tells me Sherwood may still be drawing steady buyer demand, especially for clean, well-priced homes.

Maumelle is different again. The March 2026 median sale price was around $320,200, slightly down 0.56% year over year, with homes averaging 65 days on market. Maumelle is generally a higher price-point market compared to North Little Rock and Sherwood, so payment sensitivity matters more. When rates are higher, buyers in higher price ranges tend to be more cautious.

The takeaway is simple: you cannot look at one headline and understand the whole market.

A buyer in North Little Rock may have a different negotiation strategy than a buyer in Sherwood. A buyer in Maumelle may need to pay closer attention to payment comfort and appraisal risk. A buyer in Little Rock needs to drill down by neighborhood because the Heights, West Little Rock, Midtown, Southwest Little Rock, and other areas do not all behave the same.

This is why local data matters.

Are home prices going down in Little Rock, North Little Rock, Sherwood, and Maumelle?

Not across the board.

Little Rock is up based on recent public data. North Little Rock is up. Sherwood is up. Maumelle is basically flat to slightly down.

But that does not mean every individual house is following the citywide trend.

A move-in ready home in a strong location can still command a fair price. A dated home with repair needs, a difficult layout, or a seller who is priced off last year’s expectations may need a different strategy.

This is where buyers need to slow down and compare the home against real comparable sales.

You need to look at recent sold homes, active competition, pending homes if available, days on market, list price history, price reductions, condition, concessions, and buyer demand in that exact price range.

Averages are helpful, but averages do not buy the house for you.

You are not buying the whole Little Rock market. You are buying one house.

Will interest rates drop enough to make waiting worth it?

Interest rates may change, but nobody can guarantee when, how much, or whether lower rates will actually make the house cheaper for you.

Freddie Mac reported the 30-year fixed mortgage rate averaged 6.53% as of May 28, 2026. That is lower than the 6.89% average reported one year earlier, but it is still high enough to keep affordability tight for many buyers.

A lower rate can absolutely help your payment. No question.

But waiting on rates comes with risk.

If rates drop, more buyers may come back into the market. More buyer demand can create more competition. That can push prices higher or reduce your ability to negotiate.

So yes, you may get a better rate later. But you may also pay more for the house, face more competition, or lose the negotiating power you have today.

That is why the question should not be, “What if rates drop?”

The better question is, “Does the house make sense at today’s payment?”

If the answer is no, do not force it.

If the answer is yes, then waiting just because rates might drop could cost you the right house.

Is it better to buy now and refinance later?

Buying now and refinancing later can work, but only if you can afford the home at today’s payment.

That is the part buyers need to understand.

You should never buy a house only because you assume you will refinance soon. A refinance is not guaranteed. Rates may not drop enough. Your credit could change. Your income could change. Your home value could change. Lending guidelines could change.

If the payment does not work today, the house probably does not work.

Now, if the payment does work today and rates improve later, refinancing may become a bonus. That is a different conversation.

But do not use a future refinance to justify a bad payment today.

That is not a plan. That is a gamble.

What if I buy now and home prices fall?

If you buy a home and prices fall shortly after, it can hurt if you need to sell quickly.

That is why your timeline matters.

If you are buying a home and planning to stay for several years, short-term market movement may not matter as much. Real estate is not meant to be treated like a stock you buy today and sell tomorrow.

But if you may need to move in six months, twelve months, or even less than two years, you need to be much more careful.

Selling a home costs money. You may have commissions, closing costs, repairs, concessions, moving expenses, and possible market changes. If you sell too quickly, you may not have enough time to build equity or recover your upfront costs.

That does not mean you can never sell before two years. Life happens.

But as a general rule, I like buyers to be comfortable owning the home for at least two years.

The two-year mark is often where homeownership starts to become more realistic from a break-even standpoint. By then, you have had more time to build equity, absorb some of the upfront purchase costs, and reduce the risk of selling too quickly and losing money.

The other side of that is rent.

If you rent for those same two years, that money is gone either way. You paid for a place to live, but you do not build ownership, equity, or potential appreciation from those payments.

That is why this decision is not just about whether buying is cheaper than renting today. It is about whether you plan to stay long enough for ownership to work.

If you are only going to be in the area for a few months, renting may make more sense.

If you are planning to stay two years or longer, buying becomes a much stronger conversation.

How do I know if I can actually afford the payment?

You know you can afford the payment when the full monthly number works without leaving you house poor.

That means you need to look beyond the mortgage payment.

Your real payment may include principal, interest, property taxes, homeowners insurance, mortgage insurance, HOA dues, utilities, maintenance, repairs, lawn care, pest control, and normal household expenses.

A lender may approve you for more than you personally feel comfortable spending.

That does not mean you need to spend the maximum.

I would rather see a buyer purchase a home they can comfortably afford than stretch into a home that makes every month stressful.

You also need money left after closing.

If buying the house wipes out every dollar you have, that is risky. Homes need maintenance. Things break. HVAC systems go out. Water heaters leak. Insurance premiums change. Property taxes can move.

The payment needs to work, but your cash cushion matters too.

What should first-time home buyers watch out for?

First-time home buyers need to watch out for focusing only on the down payment and forgetting about the full cost of buying and owning the home.

A lot of buyers ask, “How much do I need down?”

That is a fair question, but it is not the only question.

You also need to understand closing costs, prepaid taxes, prepaid insurance, inspections, appraisal fees, moving costs, utility deposits, repairs, furniture, appliances, and cash reserves after closing.

You also need to understand what happens after your offer is accepted.

The process does not stop when you go under contract. You still have inspections, repair negotiations, appraisal, loan underwriting, title work, homeowners insurance, final walkthrough, closing documents, and funding.

That is where preparation matters.

A first-time buyer does not need to know everything before starting. But they do need the right people helping them understand the process before they are under pressure to make fast decisions.

When does waiting make sense?

Waiting makes sense when the numbers do not work.

If your payment is too high, your income is unstable, your credit needs work, your debt is too high, or you do not have enough cash left after closing, waiting may be the smarter move.

Waiting can also make sense if you are not sure where you want to live or you may need to move again quickly.

Buying just to buy is not smart.

If you are not ready, you are not ready. There is nothing wrong with using the next few months to improve your credit, save more money, pay down debt, research neighborhoods, or get clear on what you actually want.

The mistake is waiting with no plan.

If you are going to wait, wait productively.

Know what needs to improve. Know how much you need to save. Know what payment range you are aiming for. Know what loan options may be available. Know what timeline makes sense.

Waiting can be smart if it puts you in a stronger position.

Waiting is a problem when it turns into fear, guessing, or hoping the market does something that may or may not happen.

When does buying now make sense?

Buying now makes sense when the numbers work and the home fits your life.

If you have stable income, a comfortable payment, enough cash reserves, a realistic timeline, and you find a home that meets your needs, buying may make sense even if the market is not perfect.

No market is perfect.

When rates were lower, buyers had more competition and prices moved quickly. When rates are higher, payments are tougher, but buyers may have more room to negotiate on certain properties.

There are tradeoffs in every market.

The opportunity right now is that some buyers are sitting on the sidelines because they are waiting for perfect conditions. That can create opportunities for buyers who are prepared, realistic, and focused on the right property.

That does not mean overpay.

It means run the numbers, compare the comps, understand the seller’s position, and make a smart offer.

In North Little Rock, that may mean looking for homes that have been sitting longer and seeing if there is room to negotiate.

In Sherwood, that may mean acting quickly when a clean, well-priced home hits the market.

In Maumelle, that may mean being extra careful with payment comfort because the median price point is higher.

In Little Rock, that may mean narrowing your search by neighborhood instead of treating the whole city as one market.

What is the biggest mistake buyers make when trying to time the market?

The biggest mistake buyers make is assuming they can perfectly time the market.

Most people cannot.

They wait for prices to drop, but then rates change. They wait for rates to drop, but then buyer competition increases. They wait for the perfect house, but then the houses they liked are gone. They wait for certainty, but real estate never gives perfect certainty.

That is why I do not believe buyers should make decisions based only on headlines.

You need to make the decision based on your numbers.

What payment are you comfortable with?

How much cash do you need to close?

How much money will you have left afterward?

How long do you plan to stay?

What is the condition of the house?

What do the comparable sales support?

Is there room to negotiate?

Are there seller concessions available?

Does the home fit your life for the next few years?

Those questions matter more than trying to guess the exact top or bottom of the market.

Bottom Line

In the Little Rock, North Little Rock, Sherwood, and Maumelle real estate markets, the decision to buy now or wait should come down to math, timing, and risk.

You should not buy just because someone tells you now is a good time.

You should not wait just because headlines make you nervous.

You should buy when the payment works, the house fits your life, your income is stable, you have enough cash reserves, and you are comfortable owning the home long enough for the numbers to make sense.

A good general rule is to think in terms of at least two years. If you may need to sell immediately, the costs of selling can put you in a bad position. But if you rent for those same two years, that money is gone either way.

Buying is not always the right move.

Waiting is not always the right move.

The right move is the one that works with your actual numbers.

Real advice. No pressure. No fluff.

Thinking about buying in Little Rock, North Little Rock, Sherwood, Maumelle, or Central Arkansas? Reach out and I can help you run the numbers before you make a move.

Zach Dunivan - Dunivan Real Estate - 501-988-3758 - [email protected]